Source Rock Royalties ($SRR.V)

Quick Review

No financial advice.

(Currency CAD$)

~ $40 million Market Cap.

~ $38 million EV

Overview

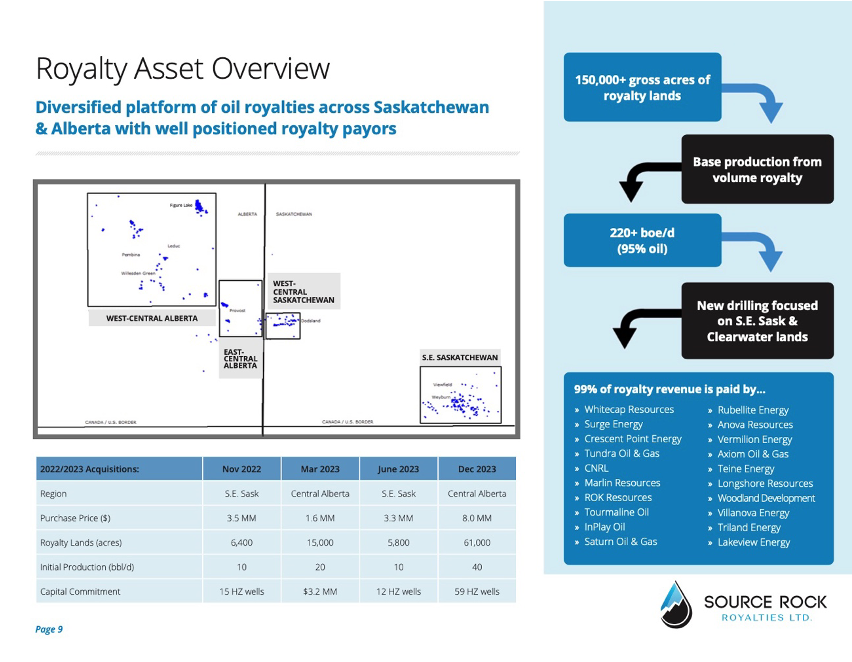

Canadian junior royalty company focused on obtaining oil & gas royalty streams in Alberta and Saskatchewan, Western Canada.

By owning the royalty stream instead of managing the operating business, the company provides shareholders exposure to crude oil without the operating costs associated to the industry.

Source Rock is focused on low-decline, high operating netback producing projects ‘with identifiable upside drilling potential’.

Its royalty streams are 100% located in the Western Canadian Sedimentary Basin (WCSB), one of the most prolific and safe jurisdictions for Oil extraction in the American continent.

Two-legs Thesis

The thesis for owning Source Rock has two legs:

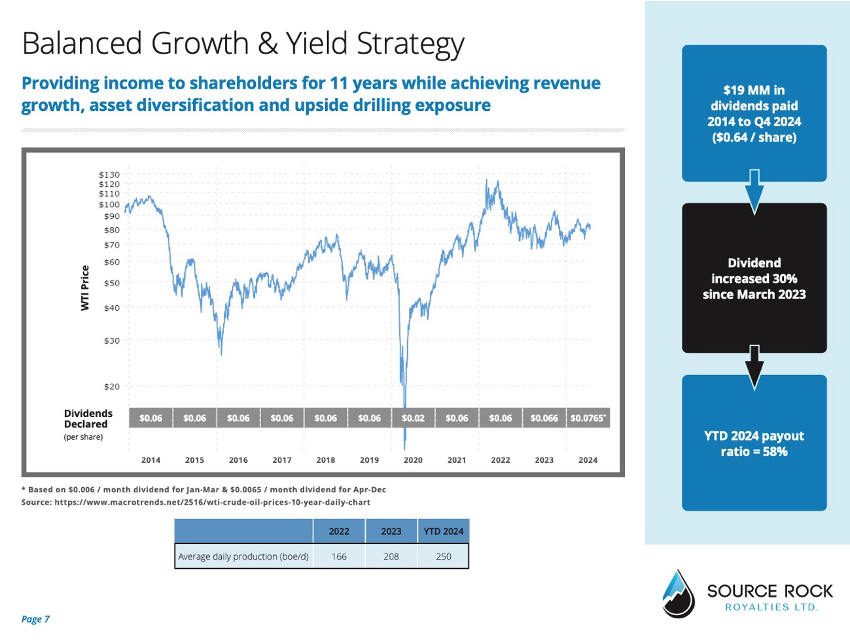

On one side, Source pays dividends, (8% dividend yield 2024E with 50%-60% payout). A royalty company, which returns money to shareholders regularly, is a good player for an income seeking strategy. In this sense, Source major shareholder is the CN Rail Pension Fund, with 21% ownership since 2014. As a fund for retirees, it makes sense to look for predictability of cash flows and have a long-term outlook.

On the other side, Source Rock gets shareholders exposure to Canadian crude oil. Why I think this fact is bullish for the long-term investor?

Buying real, scarce and desirable assets

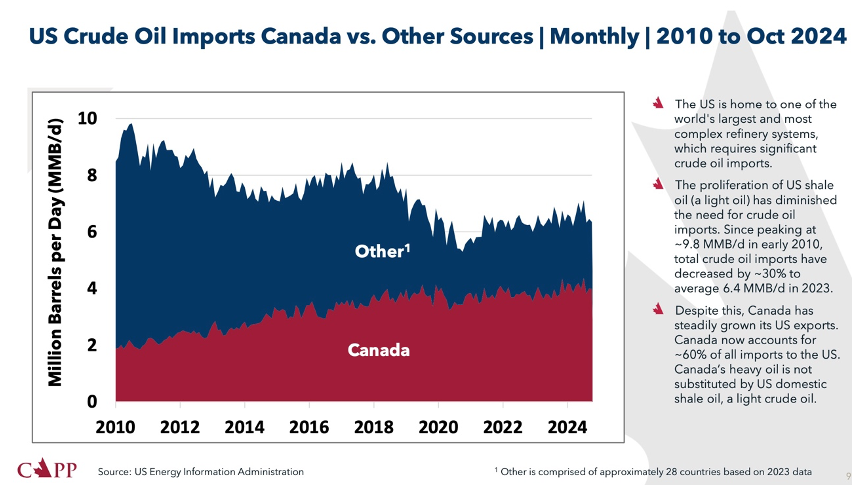

Canadian Oil mainly flows south through pipes to the USA. Almost 98% of all crude oil exported from Canada goes this way. Because the country only has one source of demand, the US, Canadian Oil trades at a discount to West Texas (WTI).

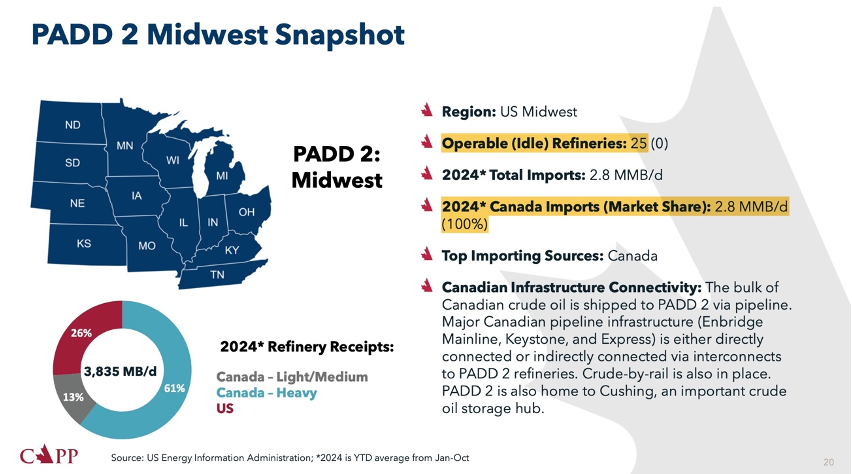

The USA divides its oil refining areas into five ‘Petroleum Administration for Defense Districts’ (PADD’s). PADD 2 (Midwest) and PADD 4 (Rocky Mountains) depend 100% on Canadian oil imports, mostly heavy oil, to complement its domestic sources. For these PADD’s, Canada is already the only supplier, and there are a limited number of refineries, meaning there’s no space to grow volumes on these areas. Nevertheless, Canada could diversify its imports by building pipelines to the coasts, and that could impact Midwest oil refineries by narrowing the differential between WTI and Canadian Oil.

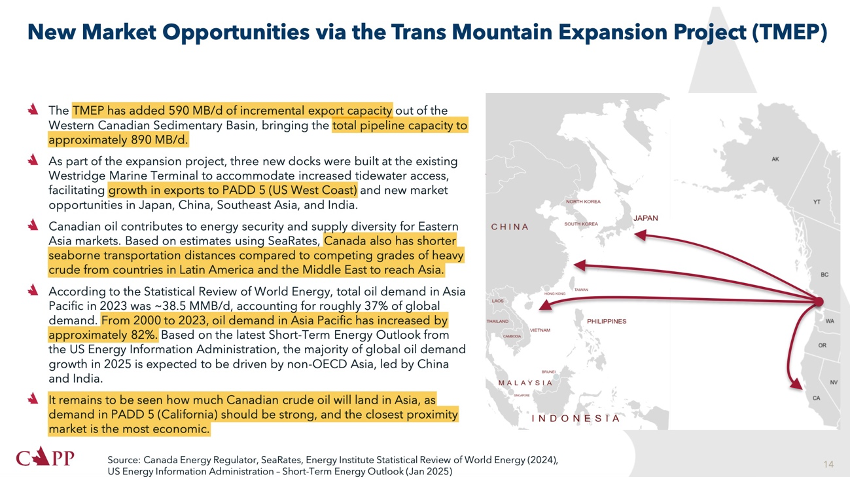

Canada already has an operating pipeline for overseas crude oil exports: the Trans Mountain Pipeline goes from Alberta to the British Columbia coast, and has seen some expansions reaching total pipeline capacity to approximately 890 Mb/d. In early February 2025, the operator of the pipeline said it was looking to expand the pipeline capacity up between 200-300 thousand b/d in an effort from Canadian business to counteract US administration tariff threats1. These pipes won’t come online on the near-term, but they will de-risk and diversify Canadian oil exports in the longer-term while making the price per barrel more competitive. Main beneficiaries of new export capacity to the coast will be Asian countries and, especially, PADD 5 (California).

Further, the possibility of a heavy oversupplied market that puts pressure on oil prices is not probable. Commodity producers follow the commodity price. On the oil sector, the ‘low hanging fruit’ as been already collected, meaning easy, cheap wells, are not more available. That’s one of the reasons why US shale oil exists. Think about it, shale is more expensive than onshore drill, but at 70$-75$ WTI it makes sense to produce. Why the hell would shale Permian producers still want to operate at 60$-50$ WTI if they’re losing money? If the price per barrel goes down, high-cost producers shut down operations, and the lack of production reduces inventories driving prices up again at some point. Further, the OPEC has no rush on increasing output, as they currently won’t allow low Brent prices and they know they have the long-term call on oil supply. OPEC needs stable prices, enough to incentivize investments but not too high to kill demand.

Moreover, the number of active drilling rigs in the US, according to Baker Hughes last report (14/02/25), displayed a -5.62% decrease on rig counts year-over-year2. And meanwhile, OECD crude oil inventories are at its lowest since 2017, meaning countries will need to build up, and Canada could respond by sending more oil overseas, should a political turn in the next elections be more friendly proactive with the national oil industry. Peak Oil is creating a plateau in supply while demand is going to increase, as transport electrification is still on its early stages.

Peers’ comparison

One common metric on the oil industry is ‘operating netback’. Essentially, it shows how much profit a company makes per barrel of oil or its equivalent after covering all the expenses directly related to extraction, transportation, and processing. Because Operating netback is a non-GAAP metric, I have calculate for Source Rock peers the same way the company reports it , so this number might differ from the ones the other companies report.

Operating netback (last quarter reported):

Source Rock Royalties (SRR.V): 70,65 $/boe

Freehold Royalties ($FRU.TO): 53,46 $/boe

Prairie Sky Royalty ($PSK.TO): 47,41 $/boe

This comparison gives a sense on the quality of the royalty streams. The differences could be due to:

Commodity mix: as Oil commands higher prices than natural gas. Prairie Sky has a much more diversified commodity mix than Source Rock (more share of natural gas).

Quality assets: lower decline rates or operating efficiencies.

Royalty rates: Source Rock could have negotiated better royalty rates.

Geographic location: SE Saskatchewan & Alberta might command higher netback. Freehold has ~30% of royalties in the US, which might bear higher operating costs.

Source Rock history and management

Source Rock Royalties was founded in 2012 by Brad Docherty, who has served as the company's Chairman, President, and Chief Executive Officer since its inception. Management and the Board of Directors have long-term experience in the oil industry and collectively own 9.5% of common shares, while approximately 5% are owned by Brad Docherty himself.

The company has been consistently paying dividends from its cash flows since 2014, only reducing them during 2020 Covid crisis.

Source Rock average daily production has increased, thanks to royalty interest acquisitions, from 166 boe/d in 2022 to 250 boe/d 2024 YTD (+50,6%). While the company is very small compared to its peers, it still has room to make accretive acquisitions that can move the needle fast.

Conclusion

My numbers are: 2024E, 5x EV/Royalty Revenue (EV/RR) or 9x Price/Funds from Operations (P/FFO), while production increases +20% YoY, although $/boe goes down -4% YoY.

Peers trade at higher multiples. Being Freehold Royalties 11x P/FFO and Prairie Sky 30x P/FFO.

While economic shocks might happen, on the long-term, oil isn’t going anywhere, as the transportation world is not ready to go full electric. Meanwhile, the US and Asian import countries will not stop demanding oil. Reserves in Canada are abundant and can supply both…if they pay the right price and Canada diversifies its clients. Overall, there’s not going to be cheap oil. Not every president desires can be fulfilled. As the ‘Depletion Paradox’3 deepens in the Permian Basin and a decade of marginal output from the US ends, the fight for the access to easy oil will increase.

https://www.reuters.com/markets/commodities/trans-mountain-says-projects-could-expand-pipeline-capacity-by-300000-bpd-2025-02-06/

https://ycharts.com/indicators/us_rotary_rigs#:~:text=US%20Rig%20Count%20is%20at,rigs%20throughout%20the%20United%20States.

https://blog.gorozen.com/blog/the-depletion-paradox

Interesting small cap without a doubt with great growth potential. Good to see that one of the major shareholders is a pension fund. I am thinking to open a position and collect the dividend. I like the royalty model. Do you know if they will also invest in water royalties like TPL?

Hello, for the moment, they only invest in oil & gas royalties in Alberta and Saskachewan. But I think they have room to grow long-term, like its bigger peers. Last year they haven't made any new aquisition due to a lot of competition and higher premiums, so they are carefull not to overpay. Nevertheless, one royalty stream is commited to open 59 new wells in the near future. And they pay dividend monthly.