Rex Concepts (REXA.WA)

Have It Your Way

Introduction

REX.WA

Market Cap. ~PLN 1.2B (~ €280M)

Rex Concepts is a Quick Service Restaurant (QSR) operator in Central Europe, who owns the exclusive rights to operate Popeyes and Burger King Restaurants in Poland, Czech Republic and Romania.

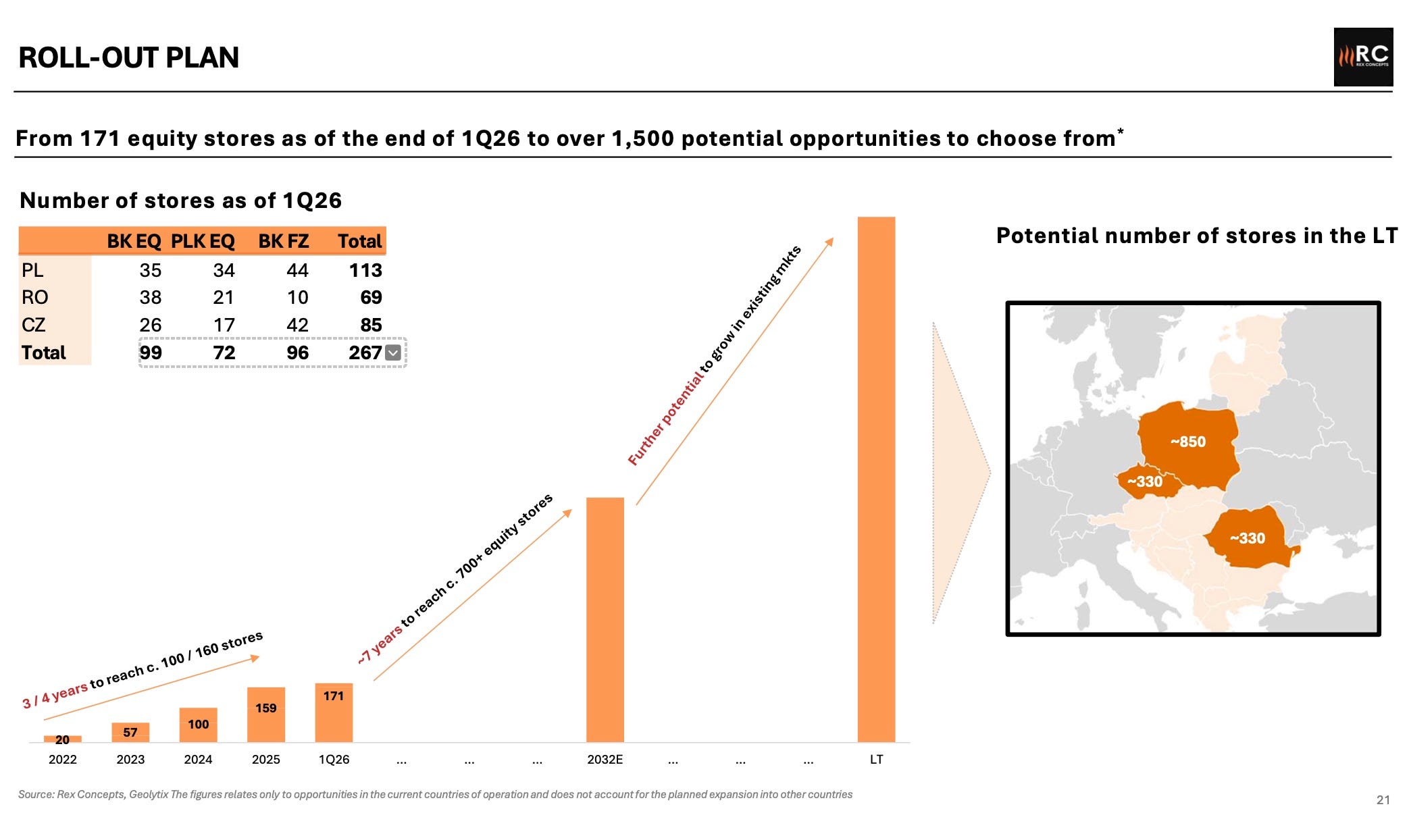

As of Q1 2026, the company has 171 owned-operated and 69 sub-franchised restaurants across the three countries mentioned.

Rex follows an owner model, where it wants to retain full control of the value chain, from central warehouse to operating the restaurants, unlike the more ‘asset-light’ franchise model followed by some competitors.

The company just IPOed this year in the Warsaw Stock Exchange with an ambitious plan to grow its equity restaurant estate and become a major player in the sector. In fact, the people involved with the company knows exactly how to do that, as some of them build what is today AmRest Holdings (EAT.WA), one of the biggest players in Central Europe on the QSR sector and exclusive operator of iconic brands like KFC, Pizza Hut or Starbucks.

Historical Numbers

Number of Restaurants:

2023 - 57

2025 - 159

Q1 2026 - 171

Revenues (owned restaurants + sub-franchise royalties):

2023 - PLN 135M

2025 - PLN 594.5M

Avg. Revenue per restaurant (owned) +30% Cagr. 2023-2025.

EBITDA:

2023 - loss of PLN -36.9M

2025 - PLN 43.4M (7.3% EBITDA margin)

Growth Plan

REX raised PLN 560 million during the IPO. Some funds went to deleveraging and most of them to expansion and growth.

IPO Targets:

70 new owned stores by end 2026.

c. 80 new equity stores openings in the mid- and long-term.

700+ equity stores by the end of 2032 (currently 171).

Tripling Revenues in the next two years.

Revenues in 2028 -2030 will at least double compared to 2027.

EBITDA margin over the long-term to reach low to mid-twenties percentage (Q1 2026 EBITDA margin of 9.8% vs. 1.9% Q1 2025).

Most of its restaurants are leased, so lease expenses should be treated as an operating cost. The target of lease payments per restaurant is between 6.0 - 9.5% of revenue in the mid-term depending on location and fit-out.

As mentioned, almost all IPO proceeds go to growing the network, opening new restaurants is estimated at an average of PLN 3.0 – 3.8M per newly opened restaurant, with a refurbishment of PLN 1.1M after 7 years of opening.

G&A as a % of revenue to decrease by 2-3 pp. over the next 2-3 years.

Actively looking for M&A targets.

Mid to long-term leverage below 3x EBITDA (currently net cash).

(Company Q1 26 presentation)

Management/Ownership

REX Invest CEE, a Luxembourg holding company owns 62% of REX shares and was the IPO selling shareholder. Then the question is: Who owns REX Invest CEE? Now things start to become more interesting. Q1 2026 report describes that “Parties Controlling or Exerting Significant Control” are Małgorzata Ewa McGovern and family, which exercise control ‘at the highest level’. At the same time, Henry McGovern is the Chairman of the Supervisory Board, so both surnames appear as significant shareholders and Board members. But who is Henry McGovern then?

Short answer: he’s the founder of AmRest Holdings (EAT.WA) the QSR operator listed in Poland since 2005. This man listed AmRest back in 2005, and during is tenure until 2019, the company’s share price appreciated by 1,500% !

Valuation

First, REX revenue per owned restaurant increased from PLN 2.1M in 2023 to PLN 3.6M in 2025 (+30% Cagr). By contrast, AmRest during Q4 2025 made a total revenue of €635.7M, and if we annualize that number (assuming no seasonality) that gives us €2.54B in Revenues. Revenue divided by de total restaurant count of 2,139 locations, gives like €1.18M revenue per restaurant, converting that number to PLN at a 4,29 EUR:PLN exchange rate, that gives around PLN 5M revenue per restaurant. Remember, REX 2025 revenue per restaurant was PLN 3.6M.

My base case assumptions are:

Revenue:

Revenue per restaurant grows 11% annually for 2 years, then 2% until 2032. That would give PLN 4.9M revenue per restaurant in 2032, slightly below AmRest numbers today.

Restaurant Count:

70 openings per year until 2032 for a total of 649 restaurants, below management targets of +700 restaurants by 2032.

Costs:

6% Restaurants costs growth annually during the first two years, then 1.5% growth annually.

2032 G&A at 6.7% of sales, in line with management targets.

Then we get to an EBITDA estimate for 2032 of PLN 600M with an 18.7% EBITDA margin, which is slightly below management targets of ‘low to mid-twenties percentage’. Then adjusting EBITDA for lease payments of PLN 249.2M ( 7.8% of sales, remember management assumes 6%-9.5% leases as a % of revenue), gives an adjusted EBITDA of PLN 351.4M.

Next step is to assume some amount of net debt by 2032. Management targets net debt to EBITDA below 3x, so I’ll assumed 2.5x. At 2032E EBITDA number, that’s around PLN 1.5B net debt. I won’t factor any share issue, as the company will use financial debt, although there’s a long term incentive plan which will grant equity to directors going forward.

Considering the exit multiple, it seems that most restaurant operators in Europe have seen its multiple compressed since 2022, due to inflation and weak consumer spending. Back in the days of Henry McGovern, AmRest traded around 10-15 times EV/EBITDA. Now its multiple has compressed to around 5x EV/EBITDA. Another comparable could be Dominos Pizza Group (DOM.L), which now trades at 10x EV/EBITDA while in the good days before 2022 traded at 15-20x.

For the base case I’ll assume 10x EV/adj.EBITDA multiple considering McGovern leadership and a slightly better consumer spending environment in Central Europe after 2030.

Base Case Summary:

Adj. EBITDA 2032E - PLN 351.4M.

Exit multiple - 10x

Net Debt - PLN 1.5B

Shares outst. - ~95.2M

Target Price: PLN 21.1

Current Price: PLN 13

Bear Case summary:

Adj. EBITDA 2032E - PLN 300.7M.

Exit multiple - 8x

Net Debt - PLN 1.5B

Shares outst. - ~95.2M

Target Price: PLN 9.5

Current Price: PLN 13

Bull Case summary:

Adj. EBITDA 2032E - PLN 400.7M.

Exit multiple - 12x

Net Debt - PLN 1.5B

Shares outst. - ~95.2M

Target Price: PLN 34.7

Current Price: PLN 13

Some important nuances here. As mentioned above, management expects that new restaurant openings require around PLN 3-3.8M initial CAPEX. If we assume PLN 3.5M CAPEX per restaurant and 70 restaurant openings /year, that’s PLN 245M growth CAPEX every year until 2032 or a total amount of PLN 1.7B, more than double the IPO proceeds (note: in Q1 2026, IPO proceeds where still not reflected on the Balance Sheet, the company went public in May 2026). In this scenario, there’s no way REX will have positive free cash flow after all CAPEX spend before 2032. Only assuming maintenance CAPEX tells another story. I’ve assumed maintenance CAPEX at around 120k-140k per restaurant, or 3% of revenues. Then FCF after maintenance CAPEX-only would become positive by 2027.

But overall, although the company has a net cash position today, management is already advising the amount of financial debt we should expect to complement the IPO raise.

Growth accelerators

M&A: To accelerate its restaurant network, REX is considering to acquire individual restaurants, groups of restaurants, or entire chains in Central Europe. EUR 20M will be set aside, intended to finance potential acquisitions by the Group.

Expansion into new geographies: The company expresses interest in geographical expansion, although no target country has been identified to date.

New product categories or launch a whole new QSR brand: Entry into new product categories (such as Pizza) and/or create a new brand.

Conclusion

This investment thesis feels kind of ‘Sidecar Investing’, where you trust an experienced management who has already succeed and created wealth for shareholders in the past. Management’s vision will require to invest a lot of money into the business, and if they succeed, catching with AmRest Holdings Market Cap its a real possibility.

REX bigger comparable peers like AmRest, Dominos Group or Greggs plc are trading at historical lows and the sector might be poised for a rebound. The question is when this will happen. Anyway, this is a growth story, and growth will take time, while the economy will do its course, do Henry McGovern and his team will keep delivering as they did before?

No financial advice, just notes from certain companies I find interesting. Please comment if you feel there’s something important to add. I would appreciate your comments. Thanks!